The World shifted over the weekend. Trump’s 100% China Tariff threat was a snap reaction to the reality is China is now the key power in global trade, and holds most of the cards. There are significant risks ahead, not the least being the AI bubble popping – which would kill US sentiment as the whole stock market edifice will trumble.

King Charles played a blinder in Windsor last night, making Trump feel regal. But the reality is Europe and the UK have difficult decisions to make. Do they remain aligned with a post-hegemonic USA slipping into autocratic polarisation, or do they seek closer Asian connections, including China? There are massive Economic and Geopolitical risks ahead.

Yesterday tremblors rocked global markets again after Israel bombed Qatar and Trump demanded Europe enact 100% tariffs on China and India. As America lashes out, It feels the world is tumbling towards chronic trade conflict and disruption – yet, yesterday the US stock market made yet another record high.

You might think China planned it this way. As it challenges the USA as global hegemon, there is panic across the West as Western Long Bond Yields hit record levels. It smells like crisis – In Bond Yields there is Truth – but you have to know how to read the market. Long bonds are weak because of inflation. Be concerned, but not fearful. Buy the short-end – cuts are coming!

The AI revolution is exceedingly expensive. It’s become a matter of who can chuck the most amount of money at it. But that’s forgetting it’s still evolving and there is little to stop it moving in new directions.

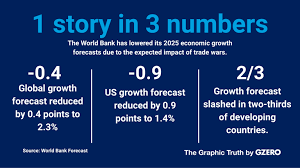

Plus, The Morning Porridge experiments with AI generated graphs!

The last 6 months has been….. interesting. The world has been shaken, stirred, and left confused, uncertain and destablised. Fantastic. Big shocks create massive opportunities. The issue for markets is understanding why, where and what they are!

Trump blinked. 42 days after “Liberation Day” China gets a 10% base tariff level, putting it on better trade terms than the EU? It was a ramble of conflicting narratives, but the reality is the US may just have averted a catastrophic trade induced crash – it will likely still experience a stagflationary shock.

The narrative in US markets grows more improbable every day. Did Trump not threaten to sack Powell last week? And aren’t massive tariffs on China a guarantee of US victory? Apparently, that was just a dream sequence, and Bobby Ewing is about to step out the shower. Confused? You will be. Welcome to Trump – The Soap.

The irresistible force of Trump has hit the immovable rock of Economic and Market Reality. The inconsistencies of Trump’s tariff policies - the centre-plank of his economic understanding - have been exposed as bogus. It begs the question – What Next? Which is why markets are braced for even more dislocation.

Up, down, shake it all about. Current markets are driven by short-term rumour and sigh about what Trump might do or say next on tariffs. However, the real threats are longer-term – how the global economy is increasingly vulnerable not just to trade and economics, but also the growing weakness and unravelling of US military might. The implications for global security could change everything.

Disclaimer

This publication is protected by US, UK and International Copyright laws. All rights reserved. No License is granted except for the subscriber’s personal use. Rights will be pursued.

The Morning Porridge is not investment advice. It is market commentary based on discussions and information gathered from multiple sources believed to be reliable. No guarantee is given for its accuracy or completeness. It is not an offer to buy, sell or solicit investments or securities. The author may have a position in companies or institutions discussed in this commentary.

If you want to know what’s really happening and why.. welcome to the Porridge.

Financial Market Insights for Thinkers!

© Morning Porridge | All Rights Reserved | Website Design & Support by Orange Pixel